Tax deadlines feel arbitrary, don’t they? March 15th for S-Corps, April 15th for individuals, October 15th for extensions. Just dates on a calendar that someone in Washington decided would work for everyone. Except they’re not arbitrary at all. These deadlines represent the IRS’s expectation that you’ll have your financial house in order by specific dates. Miss them, and you’re not just facing late fees—you’re signaling to tax authorities that your business operations might need closer scrutiny. The cost of late tax filing extends far beyond simple penalty calculations. It affects your business credit, your relationships with lenders, your eligibility for certain programs, and even your ability to operate in some industries. Understanding why timely filing matters—and implementing systems to ensure it happens consistently—can save your business thousands of dollars and countless headaches. The Domino Effect of Late Tax Filing When businesses file taxes late, the consequences cascade through multiple areas of their operations. The initial penalty might seem manageable, but the secondary effects often prove more costly than the original fine. Late filing creates a paper trail that follows your business for years, affecting everything from loan applications to vendor relationships. Immediate Financial Penalties The IRS doesn’t negotiate on late filing penalties. File your business tax return even one day late, and you’ll face a penalty of 5% of the unpaid tax amount for each month or part of a month that your return is late, up to a maximum of 25%. For a business owing $10,000 in taxes, that’s $500 per month in penalties alone—money that could have been invested back into your business operations. State tax agencies follow similar penalty structures, often with their own additional fees and interest charges. Some states impose flat penalty fees regardless of the tax amount owed, meaning even businesses with minimal tax liability face significant penalty expenses for late filing. The combination of federal and state penalties, plus interest that compounds daily, can quickly turn a manageable tax bill into a financial crisis. Small businesses operating on tight margins find these unexpected penalty expenses particularly damaging to their cash flow and growth plans. Credit and Lending Implications Most business owners don’t realize that tax filing compliance affects their business credit scores and lending eligibility. Lenders routinely request tax transcripts as part of loan applications, and late filing patterns signal financial disorganization to potential creditors. Banks interpret consistent late filing as an indicator of poor cash flow management and operational inefficiency. SBA loans, business lines of credit, and equipment financing all require recent tax returns as part of the application process. Late filing can delay these applications significantly, potentially causing businesses to miss growth opportunities or forcing them to seek more expensive alternative financing. Compliance and Legal Issues Late tax filing can trigger increased scrutiny from tax authorities, making your business more likely to face audits or compliance reviews. The IRS and state agencies use filing compliance as one factor in determining which businesses to examine more closely. A pattern of late filing essentially puts your business on their radar for future attention. For businesses in regulated industries, tax filing compliance often connects to licensing requirements. Late filing can jeopardize professional licenses, contractor certifications, or industry-specific permits that are essential for continued operations. Understanding Tax Filing Deadlines: More Than Just Calendar Dates Tax deadlines aren’t random dates—they’re carefully structured to align with business cycles, government revenue needs, and administrative processing requirements. Understanding the logic behind these deadlines helps businesses plan more effectively and avoid the rush that leads to errors and last-minute stress. Business Entity Deadlines Vary for Good Reasons Different business structures face different filing deadlines because they have different tax implications and complexity levels. S-Corporations file by March 15th because their tax information flows through to individual owners’ tax returns, which are due April 15th. This timeline gives shareholders time to receive their K-1 forms and complete their personal returns. C-Corporations filing calendar year returns face the same March 15th deadline, but their tax obligations differ significantly from pass-through entities. Partnerships also file by March 15th, but their complexity often requires more preparation time than other entity types due to multiple partners and varying ownership percentages. Sole proprietorships and single-member LLCs file with individual tax returns by April 15th, but this apparent simplicity can be deceiving. These business owners often have the most complex preparation requirements because they must integrate business and personal tax information on the same return. Extension Options and Their Limitations Tax filing extensions provide additional time to file returns but don’t extend payment deadlines. This critical distinction causes confusion for many business owners who assume extensions provide relief from both filing and payment obligations. The IRS expects estimated tax payments by the original deadline regardless of extension status. Extensions are useful when businesses need additional time to gather documentation or resolve complex tax issues, but they’re not a solution for cash flow problems or poor planning. Businesses that consistently rely on extensions may face additional scrutiny and should examine their financial management processes. Some states don’t automatically honor federal extensions, requiring separate state extension filings. Multi-state businesses must track different requirements for each jurisdiction where they operate, adding complexity to their compliance obligations. The Strategic Benefits of Timely Filing Beyond avoiding penalties, timely tax filing provides strategic advantages that help businesses operate more efficiently and position themselves for growth opportunities. These benefits often outweigh the costs of maintaining organized financial records and meeting filing deadlines. Improved Cash Flow Management Businesses that file taxes on time have better visibility into their annual tax obligations, enabling more accurate cash flow forecasting and budgeting. This predictability helps with strategic planning and reduces the need for emergency financing to cover unexpected tax bills or penalties. Timely filing also expedites refund processing when businesses are entitled to refunds from overpaid estimated taxes or credits. These refunds can provide important cash flow boosts, particularly for seasonal businesses or those making significant investments in equipment or expansion. Enhanced Business Credibility Consistent timely filing

Payroll Management: Why Getting It Right Matters More Than You Think

You hired your first employee. Congratulations! Now you’re staring at payroll software, tax tables, and government forms that make your head spin. What seemed like a simple task—paying someone for their work—has suddenly become a bureaucratic maze. Welcome to payroll management. Where one mistake can cost you thousands in penalties, upset your best employees, and turn your HR department into a crisis management center. But here’s the good news: Once you understand the system, payroll becomes predictable, manageable, and even strategic for your business growth. Let’s break it all down. Why Payroll Is More Complicated Than Writing a Check Think payroll is just about calculating hours and cutting checks? That was true maybe 30 years ago. Today’s payroll involves federal taxes, state taxes, local taxes, unemployment insurance, workers’ compensation, benefits deductions, retirement contributions, and a dozen other variables that change regularly. Miss one component? The penalties add up fast. The IRS doesn’t accept “I didn’t know” as an excuse. Neither do state tax agencies. Or your employees when their paychecks are wrong. The Real Cost of Payroll Mistakes Let’s talk about what happens when payroll goes wrong. Because it will go wrong if you’re winging it. Federal Penalties That Hurt Late payroll tax deposits trigger automatic penalties. We’re talking 2% to 15% of the unpaid amount, depending on how late you are. File your quarterly 941 forms late? That’s another penalty. Misclassify an employee as a contractor? The IRS will come after you for unpaid payroll taxes, plus penalties and interest. These aren’t small amounts. A business with 10 employees can face thousands in penalties for seemingly minor mistakes. Employee Trust Issues Your employees depend on accurate, timely paychecks. Mess this up consistently, and you’ll lose good people. Incorrect tax withholdings create headaches at tax time. Missed benefit deductions cause insurance coverage gaps. Late payments create financial stress for your team. Word spreads. Your reputation as an employer suffers. Recruiting becomes harder. Compliance Nightmares Every state has different requirements. Some cities add their own taxes. Worker classification rules vary by jurisdiction. New employees trigger reporting requirements. Terminated employees need final pay within specific timeframes. The complexity multiplies as you grow. What works for 5 employees breaks down at 25 employees. Understanding Payroll Components: The Building Blocks Before diving into solutions, let’s understand what you’re actually managing. Gross Pay Calculation This seems straightforward until you factor in overtime rules, different pay rates, bonuses, commissions, and piece-rate work. Salaried employees get complicated when they work partial periods or take unpaid leave. Hourly employees require accurate time tracking and proper overtime calculations. Tax Withholdings: Federal, State, and Local Federal income tax withholding depends on the employee’s W-4 form, pay frequency, and current tax tables. FICA taxes (Social Security and Medicare) are straightforward percentages, but they have wage limits that change annually. State income taxes vary dramatically. Some states have no income tax. Others have complex withholding requirements. Local taxes add another layer. Cities, counties, and school districts can all impose payroll taxes. Benefits and Deductions Health insurance premiums, retirement contributions, union dues, garnishments, parking fees—the list goes on. Some deductions are pre-tax (reducing taxable income). Others are post-tax. Some have annual limits. Getting the order of operations wrong affects tax calculations and employee net pay. Employer Taxes and Contributions You don’t just withhold taxes—you also pay employer portions of FICA, unemployment insurance, and workers’ compensation. These employer taxes add roughly 7-10% to your total payroll costs. States require unemployment insurance contributions based on your experience rating. New businesses start at higher rates. The Payroll Process: Step by Step Successful payroll requires consistent processes and careful attention to detail. Data Collection and Verification Time tracking for hourly employees needs to be accurate and complete. Missed punches, overtime approvals, and schedule changes all affect payroll. Salary adjustments, new hires, terminations, and benefit changes must be processed timely. Employee information updates (address changes, tax withholding adjustments, direct deposit changes) need immediate attention. Calculation and Review Payroll software helps, but you still need to review calculations for accuracy. Look for unusual amounts, negative deductions, or missing information. Verify overtime calculations comply with federal and state rules. Check that tax withholdings match current tables and employee elections. Payment Processing Direct deposit is standard, but you need backup procedures for new employees or banking issues. Pay stubs must include required information: gross pay, deductions, net pay, year-to-date totals. Timing matters. Some states require payment within specific periods after the pay period ends. Tax Deposits and Reporting Federal payroll taxes usually deposit electronically within 1-4 business days after the pay date. State tax deposit requirements vary but follow similar timelines. Quarterly and annual reporting requirements include forms 941, 940, W-2s, and various state forms. Payroll Technology: Your Best Friend or Worst Enemy The right payroll software can automate most of the complexity. The wrong choice creates more problems than it solves. What to Look for in Payroll Software Automatic tax updates keep you current with changing rates and requirements without manual intervention. Direct deposit capabilities reduce check processing and improve employee satisfaction. Time tracking integration eliminates double data entry and reduces errors. Benefits administration handles insurance premiums, retirement contributions, and other deductions. Reporting features generate required government forms and management reports. Customer support matters when you’re dealing with payroll deadlines and compliance questions. Popular Payroll Solutions QuickBooks Payroll integrates with accounting software many businesses already use. Good for basic payroll needs. ADP and Paychex offer full-service solutions including tax filings and compliance support. Higher cost but less hands-on management required. Gusto provides modern interfaces and good small business features at competitive pricing. The key is matching the solution to your business complexity and growth plans. Integration Considerations Your payroll system should connect with your accounting software to eliminate duplicate data entry. Time tracking systems need to feed payroll calculations accurately. Benefits administration platforms should integrate to handle deduction changes automatically. HR systems require payroll integration for new hires, terminations, and employee data updates. Common Payroll Mistakes and How to

The Complete Guide to Bookkeeping & Financial Management for Small Businesses

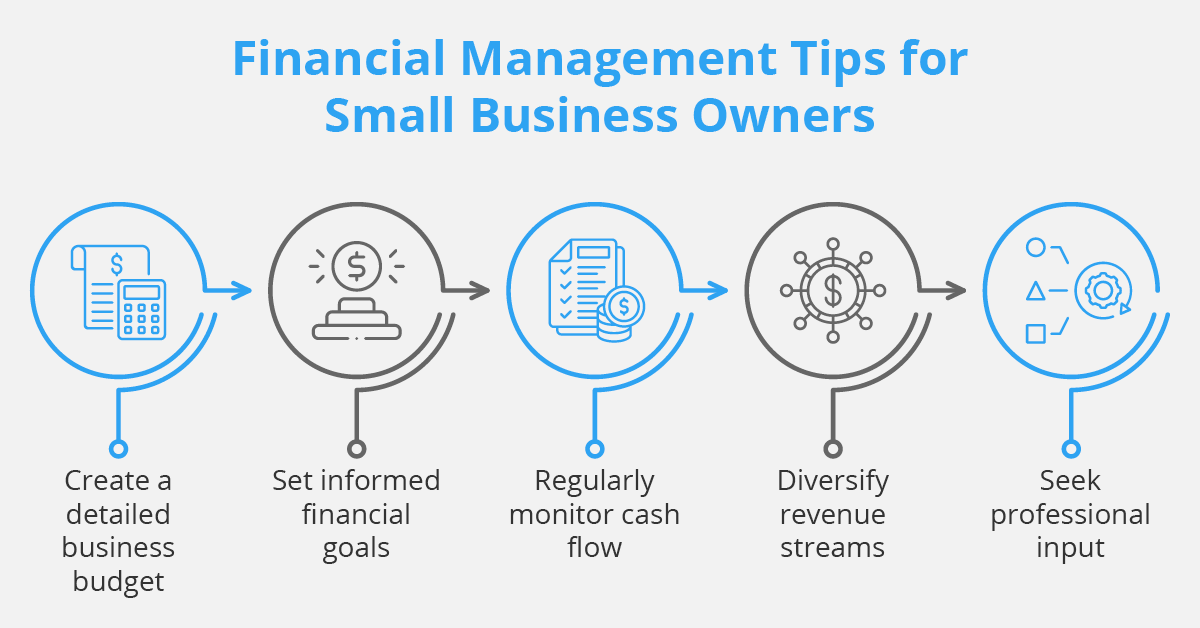

Your business is growing. Orders are coming in. Customers love what you’re doing. But there’s a problem lurking in the background. You have no idea if you’re actually making money. Sound familiar? You’re not alone. Most small business owners can tell you their sales numbers off the top of their head, but ask them about their profit margins, cash flow, or upcoming tax obligations? That’s where things get fuzzy. Here’s the truth: You can’t manage what you don’t measure. And without proper bookkeeping and financial management, you’re essentially flying blind in a storm. Let’s fix that. Why Your Business Needs More Than Just “Good Enough” Bookkeeping Think bookkeeping is just about keeping receipts and tracking expenses? Think again. Proper financial management is the difference between businesses that scale successfully and those that collapse under their own growth. It’s the difference between confident decision-making and constant financial anxiety. Consider this: 82% of small businesses fail due to cash flow problems. Not lack of customers. Not bad products. Cash flow. The businesses that survive and thrive? They have systems in place that give them crystal-clear visibility into their financial health at all times. The Real Cost of Financial Chaos Before we dive into solutions, let’s talk about what’s really at stake when you ignore proper financial management. Money Walking Out the Door Without organized expense tracking, you’re probably overpaying on taxes. We’re talking about thousands of dollars in legitimate business deductions that never get claimed because they’re buried in disorganized records. Business meals? Home office expenses? Travel costs? Professional development? All deductible. All commonly missed. The Cash Flow Rollercoaster You might have $100,000 in outstanding invoices but only $500 in the bank to cover payroll next week. Without proper systems, you’re always reacting to financial emergencies instead of preventing them. This reactive approach kills businesses. Even profitable ones. Growth Opportunities Slipping Away Banks want to see clean financial statements before they’ll consider loans. Investors need proof of financial stability before they’ll write checks. Poor bookkeeping doesn’t just look unprofessional—it blocks access to the capital you need to grow. Building Your Financial Foundation: The Essentials Ready to get your financial house in order? Here’s where to start. Your Chart of Accounts: Keep It Simple, Keep It Useful Your chart of accounts is basically a filing system for your money. Too simple, and you won’t get useful insights. Too complicated, and you’ll abandon it within a month. Here’s what works for most small businesses: Income streams: Break these down by major product or service lines. You want to know which parts of your business actually make money. Expenses: Group them logically. Office supplies, marketing, professional services, rent. Keep it specific enough to be useful, general enough to be manageable. Assets and liabilities: Track what you own and what you owe. This matters more than you think, especially if you ever want to sell or get financing. The key? Design it once, stick with it consistently. The Monthly Financial Check-Up Most business owners check their bank balance daily but review their actual financial performance never. Big mistake. Set aside time every month for a financial review. Same time, same process, every month. What are you looking for? This monthly habit catches problems while they’re still small and manageable. Expense Tracking That Actually Works The best expense tracking system is the one you’ll actually use consistently. Here’s what works in the real world: Snap photos immediately. Receipt in hand? Photo in phone. Don’t wait. You’ll forget what that $73 charge was for if you wait until Friday. Use automation. Connect your business accounts to your accounting software. Let technology do the heavy lifting of data entry. Weekly reviews. Spend 30 minutes every Friday categorizing expenses and flagging anything unusual. This prevents year-end data entry marathons. Separate business and personal expenses. This isn’t just good practice—it’s essential for tax compliance and legal protection. Financial Management: Where Strategy Meets Numbers Once your bookkeeping basics are solid, you can start using your financial data strategically. This is where business growth really accelerates. Cash Flow Forecasting: Your Financial GPS Cash flow forecasting isn’t about predicting the future perfectly. It’s about spotting potential problems early enough to solve them. Start simple. Create a 13-week rolling forecast that tracks: Update it weekly. Even basic forecasting can prevent most cash flow crises by giving you advance warning of tight periods. The Numbers That Actually Matter Not all metrics are created equal. Focus on the ones that drive real business decisions: Gross profit margin: This tells you how efficiently you deliver your product or service. If it’s declining, you have a pricing or cost problem. Customer acquisition cost: How much do you spend to get each new customer? Compare this to customer lifetime value to ensure you’re growing profitably. Days to collect payment: How long does it take customers to pay you? Longer collection periods strangle cash flow. Burn rate: How much cash do you consume monthly? Critical for businesses not yet profitable or planning major investments. Track these monthly. Watch for trends. Act when you see problems developing. Budgeting Without the Headaches Forget complex budget spreadsheets that take hours to maintain. Start with a simple framework: Review monthly. Adjust based on what you learn. The goal isn’t perfection—it’s awareness and intentional spending decisions. Technology: Your Financial Management Ally The right tools can transform financial management from a dreaded chore into a streamlined process that actually helps your business. Choosing Accounting Software For most small businesses, cloud-based solutions like QuickBooks Online or Xero provide the right balance of features and simplicity. Look for: Don’t overcomplicate this decision. Pick something, learn it well, and use it consistently. Automation Opportunities Every minute you save on routine bookkeeping is a minute you can invest in growing your business. Automate these tasks: Start with one automation, master it, then add another. Common Mistakes That Cost Money Even well-intentioned business owners fall into these traps: Mixing Personal and Business Finances This creates bookkeeping nightmares and can jeopardize your

The Impact of Global Tax Reforms on Small Businesses

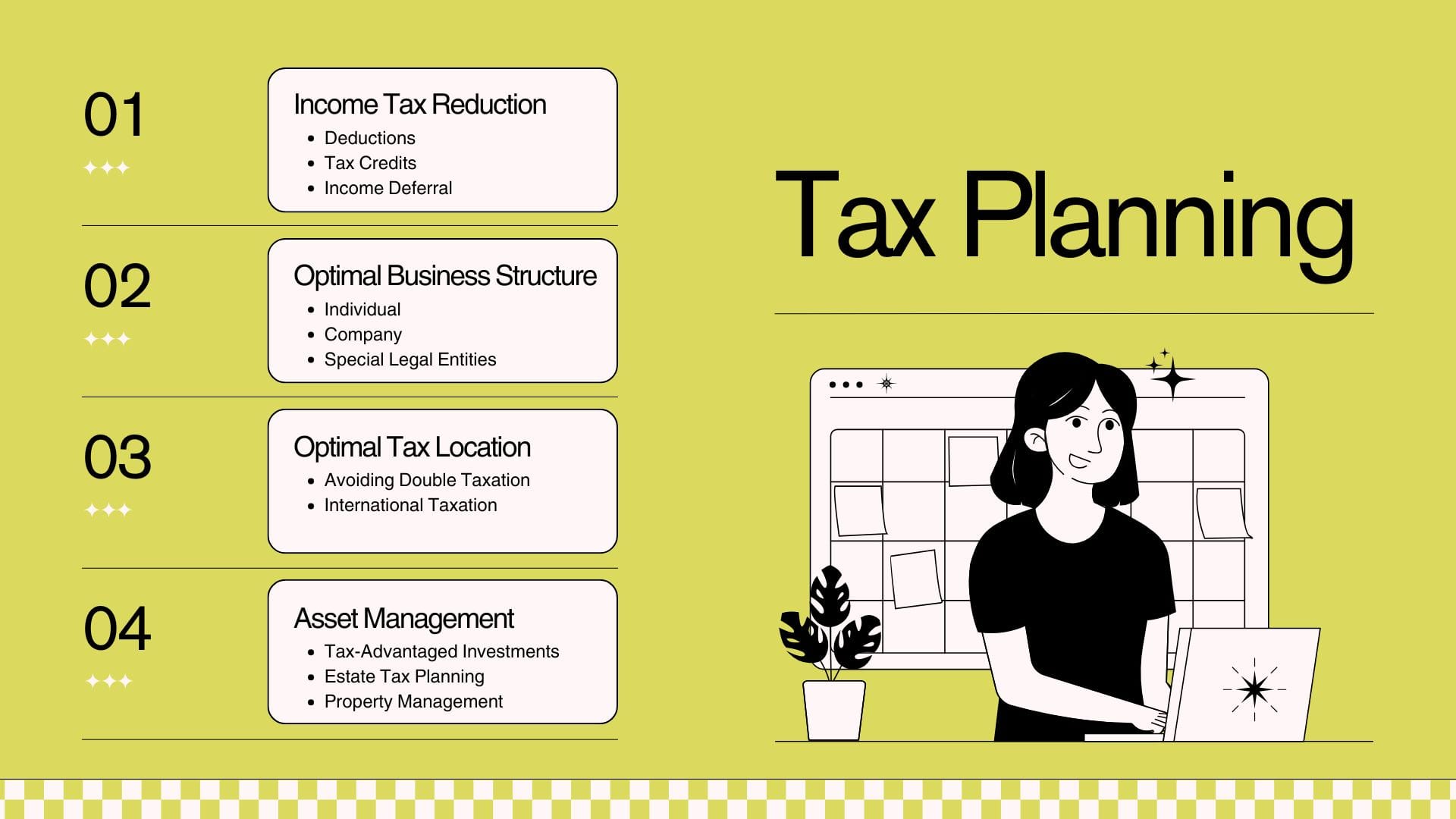

International tax reforms are transforming the economic environment, affecting companies across the spectrum. For small enterprises, these reforms present a mix of challenges and opportunities. Unlike large corporations that can swiftly adjust due to their ample resources, small businesses typically function with limited budgets and reduced access to specialized advice, making the effects of tax reforms especially significant. This article explores the essential elements of international tax reforms, their effects on small enterprises, and approaches to successfully maneuver through the changing tax landscape. Understanding Global Tax Reforms Tax reforms generally seek to tackle challenges like economic disparity, tax evasion, and the enhancement of revenue streams. In recent times, international tax reforms have been motivated by the necessity to update antiquated systems in order to adapt to shifts in the global economy, including digital advancements and international trade. Key Drivers of Global Tax Reforms Implications for Small Businesses The effects of global tax reforms on small businesses vary depending on their size, industry, and geographic location. Here’s a breakdown of the key impacts: 1. Compliance Costs and Administrative Burden Tax reforms frequently bring about new requirements for reporting and documentation. For small businesses with limited resources, adapting to these changes can be both time-consuming and financially burdensome. For example: • Digital Sales Taxes: Companies selling products or services online may have to navigate a patchwork of tax regulations across different countries or states. • Transfer Pricing Regulations: Small businesses involved in international trade must comply with intricate rules, often necessitating expertise that they may not possess. 2. Increased Tax Liabilities Changes such as the introduction of minimum corporate tax rates and the curtailment of tax havens can result in increased tax obligations for small businesses. This is especially relevant for those that depend on low-tax jurisdictions to maximize profits. For instance: • A small e-commerce enterprise exporting products to various countries may encounter heightened tax responsibilities due to new international tax agreements. • Environmental taxes could raise expenses for businesses operating in energy-intensive sectors. 3. Opportunities Through Incentives Not all reforms are negative. Numerous governments offer tax incentives aimed at fostering innovation, sustainability, and local job creation. Examples include: • R&D Tax Credits: Small businesses that invest in research and development may qualify for tax deductions or rebates. • Green Energy Subsidies: Shifting to renewable energy sources or implementing sustainable practices can alleviate tax pressures. By aligning their strategies with these incentives, small businesses can transform reforms into avenues for growth. 4. Competitive Disadvantages Although global tax reforms aim to create a more equitable environment, small businesses frequently find it challenging to compete with larger corporations that benefit from economies of scale. For instance: • A multinational corporation can invest in a dedicated team of tax experts to enhance its tax strategy, whereas a small business may not have access to similar financial resources. • The compliance requirements associated with global standards can place a heavier burden on smaller enterprises, distracting them from their primary business functions. Sector-Specific Impacts 1. E-Commerce and Digital Services As digital marketplaces expand, numerous countries are implementing taxes on online transactions. Small e-commerce enterprises must adapt to new regulations, including value-added tax (VAT) on internationally sold digital products. For instance, a small app development firm offering software subscriptions worldwide is now required to register for VAT in several jurisdictions, leading to increased complexity and expenses. 2. Manufacturing and Exporters Manufacturers engaged in global supply chains may be impacted by tariffs, import/export duties, and carbon taxes designed to mitigate environmental effects. For example, a small furniture manufacturer exporting to Europe could incur higher costs due to carbon border adjustment measures. 3. Startups and Innovation-Driven Businesses Startups frequently take advantage of tax incentives aimed at fostering innovation, such as grants and research and development credits. However, they may also face challenges related to global tax regulations that necessitate comprehensive documentation and compliance. Strategies for Small Businesses to Navigate Tax Reforms Adapting to global tax reforms requires a proactive approach. Here are strategies to help small businesses stay ahead: 1. Invest in Tax Expertise Engaging a tax professional or consulting with an expert can help small businesses avoid expensive errors. Outsourcing tax compliance tasks can also allow more time to concentrate on growth. 2. Embrace Technology Utilizing tax technology solutions, such as accounting software equipped with compliance tools, can streamline processes like tax calculation and reporting. Automation minimizes the risk of mistakes and ensures timely submissions. 3. Stay Informed Consistently tracking changes in tax legislation is essential. Subscribing to updates from tax authorities or industry organizations can aid businesses in maintaining compliance. 4. Leverage Tax Incentives Identify and utilize available tax credits, deductions, and grants for activities such as research and development, hiring, or implementing sustainable practices. 5. Plan for Higher Costs Reforms may result in increased tax obligations. Small businesses should factor these potential expenses into their financial planning and pricing strategies. Global Examples of Tax Reform Impacts 1. The European Union’s VAT Rules In 2021, the EU established new VAT regulations mandating that businesses selling products to EU consumers collect VAT at the time of sale. This reform removed the VAT-free threshold for small enterprises, thereby heightening compliance obligations. Impact: A small craft business in the UK selling to EU clients is now required to register for VAT within the EU, leading to increased administrative expenses. 2. The U.S. Corporate Tax Reforms The U.S. enacted substantial modifications through the Tax Cuts and Jobs Act of 2017, which included a lowered corporate tax rate and revised international taxation rules. While some small enterprises enjoyed the benefits of reduced rates, those involved in international trade encountered additional complexities. Conclusion Global tax reforms offer a blend of challenges and opportunities for small businesses. While the concerns regarding compliance costs and increased liabilities are significant, these reforms also create avenues for new incentives and growth opportunities. By staying updated, utilizing technology, and seeking professional advice, small businesses can not only endure but also prosper in the changing tax environment. Proactive

The Importance of Financial Forecasting in Uncertain Times

Financial forecasting involves projecting a company’s future financial performance by examining past data, prevailing economic conditions, and particular business strategies. During periods of uncertainty—such as economic recessions, global health crises, or changing market conditions—financial forecasting takes on heightened importance. It equips business leaders with a framework for making informed decisions, mitigating risks, and maintaining resilience. This article will explore the significance of financial forecasting in uncertain times and detail essential steps for developing a comprehensive forecasting strategy. 1. Anticipating Risks and Managing Cash Flow In periods of economic instability, effective cash flow management becomes essential. Organizations may face the risk of cash flow deficits due to reduced sales, postponed payments, or unforeseen expenditures. By forecasting future cash flows, a business can pinpoint potential deficiencies and devise appropriate strategies. For instance, if projections indicate an impending cash shortfall, the organization might opt to secure a credit line, postpone non-essential acquisitions, or optimize expenditures to protect its cash reserves. An anticipatory approach to cash flow forecasting empowers a business to sustain liquidity and maintain operations, even amidst challenging economic conditions. 2. Guiding Strategic Decision-Making Financial forecasting serves as a crucial tool for leaders, aiding them in identifying which strategic avenues to explore. During uncertain times, it is vital for decision-makers to visualize various potential scenarios, encompassing best-case, worst-case, and most-likely outcomes. Scenario-based forecasting enables organizations to evaluate different strategies and select the one that mitigates risk while seizing available opportunities. For example, if sales forecasts are ambiguous, a business may choose to scale back certain initiatives or postpone expansion efforts to conserve resources. Conversely, if forecasts indicate strong demand, the organization might opt to enhance marketing initiatives to capture a greater market share. Thus, forecasting provides a systematic framework for assessing strategic choices, ensuring that decisions are informed by data rather than mere intuition. 3. Ensuring Efficient Budget Allocation A robust financial forecast identifies the optimal allocation of resources for a company to maximize its outcomes. In times of uncertainty, it is crucial to prioritize expenditures and implement strategic reductions when needed. Forecasting assists organizations in discerning which departments or initiatives warrant increased funding, and which may require budgetary constraints. For instance, if a forecast indicates a potential decline in demand for a particular product line, a company might opt to decrease production and redirect funds to more stable or expanding product lines. Thus, financial forecasting empowers businesses to adjust their budgets in response to evolving market dynamics. 4. Supporting Investor Relations and Stakeholder Confidence Investors and stakeholders closely observe a company’s capacity to manage uncertain conditions, as their financial commitments are often linked to the organization’s economic well-being. By offering stakeholders a transparent, data-informed financial outlook, the company can instill confidence that it is taking proactive measures to maintain fiscal stability. Clear forecasting fosters trust and assurance, demonstrating the organization’s readiness to address potential challenges. Additionally, providing regular updates to forecasts in light of evolving circumstances can further bolster investor confidence, reflecting the company’s dedication to adaptability and resilience. 5. Enabling Workforce Stability and Operational Continuity In times of uncertainty, employee morale and productivity may decline if there is a belief that the company faces significant risks. Actions such as layoffs, salary reductions, or temporary shutdowns can undermine employee confidence, negatively impacting productivity. Financial forecasting enables a company to prepare for various scenarios, allowing it to sustain a stable workforce even in difficult times. By implementing a forecast-based contingency plan, a company can prevent abrupt workforce reductions and effectively communicate its long-term vision to employees, fostering a sense of stability and enhancing morale. The continuity of operations is reliant on this workforce stability, underscoring the importance of forecasting as a strategic tool for long-term planning. 6. Assessing Market Opportunities and Competitive Positioning Economic disruptions frequently alter market dynamics, presenting both obstacles and prospects. Financial forecasting enables businesses to identify these emerging opportunities and strategically position themselves. For example, if a forecast indicates that rivals are reducing their operations, a company may opt to take advantage of this situation to increase its market share. By analyzing demand trends, pricing variations, and changes in consumer behavior, a business can remain flexible and proactive, leveraging market shifts ahead of its competitors. Key Steps to Develop a Robust Financial Forecast To optimize financial forecasting during periods of uncertainty, organizations must adopt a systematic methodology. The following steps are crucial: Challenges in Financial Forecasting During Uncertain Times Financial forecasting in uncertain times comes with its share of challenges. The main difficulties include rapid changes in market conditions, unpredictable consumer behavior, and fluctuating economic indicators. To navigate these challenges, companies should stay flexible, update forecasts frequently, and rely on multiple data sources. Moreover, it’s essential to avoid over-reliance on any single data point or assumption. In volatile markets, it’s easy for forecasts to become outdated quickly, so businesses must keep an open mind and adapt their models as new information becomes available. Conclusion In times of uncertainty, financial forecasting serves not merely as a planning instrument but as a vital resource that steers organizations through difficult circumstances. By identifying potential risks, informing strategic choices, managing cash flow, and sustaining confidence among investors and employees, forecasting empowers businesses to remain resilient and proactive. Organizations that emphasize financial forecasting are more adept at adjusting to evolving conditions, capitalizing on new opportunities, and emerging more robustly.

The Essential Guide to Starting a Bookkeeping Business

Small firms and entrepreneurs are increasingly looking for expert financial management assistance in the fast-paced economy of today. For those who are thinking about launching a bookkeeping firm, this offers a substantial possibility. Bookkeeping can be a successful and fulfilling job, regardless of whether you’re seeking for part-time or full-time work. This post will walk you through the crucial actions and factors to take into account when starting a profitable bookkeeping firm.The methodical documentation of financial transactions, encompassing everything from sales and purchases to receipts and payments, is known as bookkeeping. Bookkeeping is concerned with accurately documenting and organizing financial information, as opposed to accounting, which is understanding and analyzing financial data. Essential Roles of Bookkeeping: Why Launch a Bookkeeping Company? High Service Demand Many startups and small enterprises lack the funds necessary to employ a full-time accountant. Consequently, they frequently seek assistance from bookkeepers. It is anticipated that the need for bookkeeping services will only increase, making this a promising business prospect. Low Initial Expenses It takes little capital to start an accounting firm. Since many bookkeepers operate from home, you don’t need a physical office, which drastically lowers overhead expenses. A computer, accounting software, and dependable internet access are usually all you need. Adaptability and Self-reliance There is freedom in bookkeeping with regard to working hours and location. For people who wish to manage job and family obligations or other commitments, this is particularly alluring. You have the freedom to choose your own clients and set your own hours as a business owner. How to Launch a Bookkeeping Company 1. Obtain the Required Knowledge and Credentials A background in accounting or finance can be helpful, but formal education is not necessarily necessary. Think about taking classes that address tax laws, accounting software, and bookkeeping concepts. Your credibility can be increased by earning a certification, such as a QuickBooks certification or becoming a Certified Bookkeeper (CB). 2. Create a plan for your business. A thorough business strategy is essential for any new endeavor. Describe your target market, pricing policy, marketing tactics, and company objectives. If you need money, a business plan will help you get it. 3. Select a Structure for Your Business Choose your company’s legal structure. Corporations, partnerships, LLCs, and single proprietorships are typical choices. It is advisable to seek advice from a lawyer or accountant because each structure has unique implications for liability, taxes, and documentation. 4. Register Your Company You must register your company with the relevant government agencies after deciding on a name and organizational structure. Getting a business license, an Employer Identification Number (EIN), and any required permissions may be part of this. 5. Make the Correct Tool Purchases Purchase dependable accounting software like Xero, FreshBooks, or QuickBooks. You may create financial reports and manage client accounts more effectively with the aid of these tools. Additionally, to improve efficiency, think about utilizing project management, time tracking, and invoicing applications. 6. Decide on Your Price Choose the pricing structure for your services. Monthly retainers, flat fees, and hourly rates are examples of common pricing structures. To establish fair pricing and make sure you give your customers value, research your local competition. 7. Establish a Powerful Internet Presence Having an online presence is essential in the current digital era. Make a polished website that lists your offerings, costs, and contact details. Think about connecting with potential customers and promoting your business on social media sites like Facebook and LinkedIn. 8. Promote Your Offerings Attracting customers requires effective marketing. Make use of both offline and internet marketing techniques. You can join business associations, go to local networking events, and give free webinars or courses on bookkeeping-related subjects. Think about going for a run online. 9. Deliver Outstanding Customer Service The secret to keeping your clients and getting referrals is to establish a solid rapport with them. Be receptive to their questions, communicate frequently, and go above and beyond to satisfy their demands. Satisfied customers are more inclined to tell others about your offerings. Obstacles You Could Face Although launching an accounting firm might be lucrative, there are a few things to think about: Competition: There may be rivalry in the bookkeeping industry. Differentiating your services through niche specialization or distinctive value propositions is crucial. Keeping Up with Regulations: Financial and tax laws are subject to periodic changes. Keeping abreast of these developments is essential to provide precise and legal services. Time management: You will have numerous responsibilities as a business owner. Effective time management is crucial since juggling administrative and customer duties can be difficult. In conclusion It can be thrilling and rewarding to launch an accounting business. You may create a profitable practice that supports the growth of small enterprises if you have the necessary abilities, resources, and tactics. Keep in mind to concentrate on developing trusting relationships, providing top-notch customer service, and consistently honing your craft. By doing this, you will improve your clients’ financial well-being in addition to expanding your business. There are plenty of opportunities for success in the bookkeeping industry, regardless of your level of experience.

IRS Final Guidance: Credit Transfers under Inflation Reduction Act

The recent release of final regulations by the Department of Treasury and the Internal Revenue Service (IRS) sheds light on the intricate rules governing the transfer of certain tax credits under the Inflation Reduction Act. This development, coupled with the Creating Helpful Incentives to Produce Semiconductors Act (CHIPs), presents taxpayers with new avenues to leverage investment and production credits for mutual benefit. A Path to Tax Efficiency Effective for tax years commencing after December 31, 2022, eligible taxpayers now have the option to transfer a portion or all of their eligible credits to unrelated taxpayers in exchange for cash payments. This move offers a strategic approach to unlock liquidity without the burden of including the cash payments in gross income or making them deductible for the unrelated taxpayers. Navigating Compliance and Opportunities However, this newfound flexibility comes with its set of compliance obligations and nuances. Special rules address scenarios involving excessive credit transfers and recapture events, outlining the tax implications and assigning responsibility appropriately. To streamline the process, the IRS mandates a pre-filing registration through an electronic portal, necessitating completion before any election to transfer credits is made. Partnerships and S Corporations: Key Players Partnerships and S corporations play a pivotal role as both eligible taxpayers and transferee taxpayers. The regulations provide tailored guidance to ensure compliance and facilitate seamless credit transfers within these entities. A Roadmap for Taxpayers While the final regulations offer clarity, understanding and implementing these rules effectively is paramount. Taxpayers navigating these complexities can refer to IRS Publication 5884 for comprehensive instructions on utilizing the pre-filing registration tool. Partnering with Zari Financials At Zari Financials, we recognize the significance of staying abreast of evolving tax regulations and leveraging them to our clients’ advantage. With our expertise and commitment to excellence, we stand ready to guide businesses through the intricacies of credit transfers and ensure compliance with IRS requirements. Contact us today to explore how we can help you unlock tax opportunities and navigate the changing landscape with confidence.

What is TWC? How to File TWC? Understanding TWC: Simplifying Tax Filing and Compliance

Introduction: Understanding and meeting Texas Workforce Commission (TWC) compliance requirements is essential for businesses operating in Texas. In this blog, we’ll break down what TWC compliance entails and how Zari Financials can assist you in filing taxes and making payments seamlessly. What is TWC Compliance? The Texas Workforce Commission oversees various labor-related matters, including unemployment taxes, wage reporting, and unemployment insurance claims. Compliance with TWC regulations ensures that businesses fulfill their obligations to employees and the state. How to File Taxes and Make Payments with TWC: Why Choose Zari Financials? Conclusion: Navigating TWC compliance doesn’t have to be complicated. With Zari Financials, you can simplify tax filing and payment processes while ensuring compliance with TWC regulations. Let us take the stress out of TWC compliance so you can focus on growing your business. Reach out to us today to learn more about our services and how we can support your business success.

2024 State Legislation on Hemp-Derived Cannabinoids Regulation

Over the last several years, there has been a dramatic increase in retail and online sales of products containing hemp-derived and synthetically created cannabinoids. As a result, an increasing number of states are poised to take legislative action this year to regulate and curb sales of these novel products. Below is a brief overview of legislation that has been introduced on the state level this year. California On February 7, 2024, Assembly Bill 2223 (AB 2223) was introduced in the California Assembly by Assembly member Cecilia Aguiar-Curry (D). Among other changes, the bill seeks to add a new term—“synthetically derived cannabinoid”—to California law, which would be defined as a substance that is derived from a chemical reaction that changes the molecular structure of any substance separated or extracted from the plant Cannabis sativa L. (excluding decarboxylation from a naturally occurring cannabinoid acid). The bill also amends the definition of “industrial hemp” to clarify that no product may contain “any synthetically derived cannabinoid.” The bill would strengthen California’s existing regulation of these substances, such as delta-8-THC, delta-10-THC, and THCA. Nebraska Nebraska Legislative Bill 999 (LB 999), introduced by Senator Teresa Ibach (R) on January 5, 2024, seeks to clarify that CBD products that contain THC above legal limits, especially synthetic delta-8-THC and similar delta compounds, are illegal under Nebraska law. The bill would also turn over regulation of hemp cultivation from the Nebraska Department of Agriculture (NDA) to the U.S. Department of Agriculture (USDA). If LB 999 does pass, the NDA director will send a formal letter to USDA rescinding the state hemp plan, and Nebraska hemp producers would then be required to apply for a license to produce hemp under the USDA production program. Florida Senate Bill 1698 (SB 1698) and House Bill 1613 (HB 1613), filed in January 2023 and January 2024, respectively, aim to restrict the delta-9-THC content in hemp products to 2 mg per serving or 10 mg per container, whichever is lower. These bills introduce the concept of “Total delta-9-tetrahydrocannabinol concentration” and set strict limits on total delta-9-THC content in hemp products, effectively banning products with high levels of THCA. Additionally, SB 1698 and HB 1613 propose to prohibit the inclusion of synthetic or naturally occurring versions of controlled substances in legal “hemp” extract. South Dakota House Bill 1125 (HB 1125), introduced on January 22, 2024, in the South Dakota legislature, aims to prohibit the sale of hemp-derived products that have undergone chemical modification or conversion. This includes compounds such as delta-8-THC and delta-10-THC, which would be classified as “chemically derived cannabinoids” under the proposed law. HB 1125 seeks to make these chemically derived cannabinoids illegal in the state, aiming to regulate the sale of hemp-derived products more strictly. As the hemp-derived cannabinoid market continues to evolve, states are taking proactive steps to ensure consumer safety and regulatory compliance. Stay informed about these legislative developments as they unfold to navigate the evolving landscape of hemp-derived products. Stay tuned to Zari Financials for further updates and insights on regulatory changes impacting the hemp industry.

Employee Retention Credit Compliance: 7 Signs of Incorrect Claims

Teaser: Discover the top seven signs of incorrect Employee Retention Credit compliance as the IRS deadline approaches. Ensure accurate claims with Zari Financials’ expert guidance. Body: As the March 22 deadline approaches, businesses are urged to scrutinize their Employee Retention Credit (ERC) claims for compliance. The IRS has heightened its scrutiny, prompting us, the experts at Zari Financials, to highlight seven red flags to watch for: Act now to rectify any improper claims through the ERC Voluntary Disclosure Program, available until March 22, 2024. Don’t miss this opportunity to correct inaccuracies and avoid penalties. Trust Zari Financials, the leading tax advisors, to guide you through Employee Retention Credit compliance. Contact us today to ensure your ERC claims are accurate and maximize your benefits.